Industries · B2B & Professional

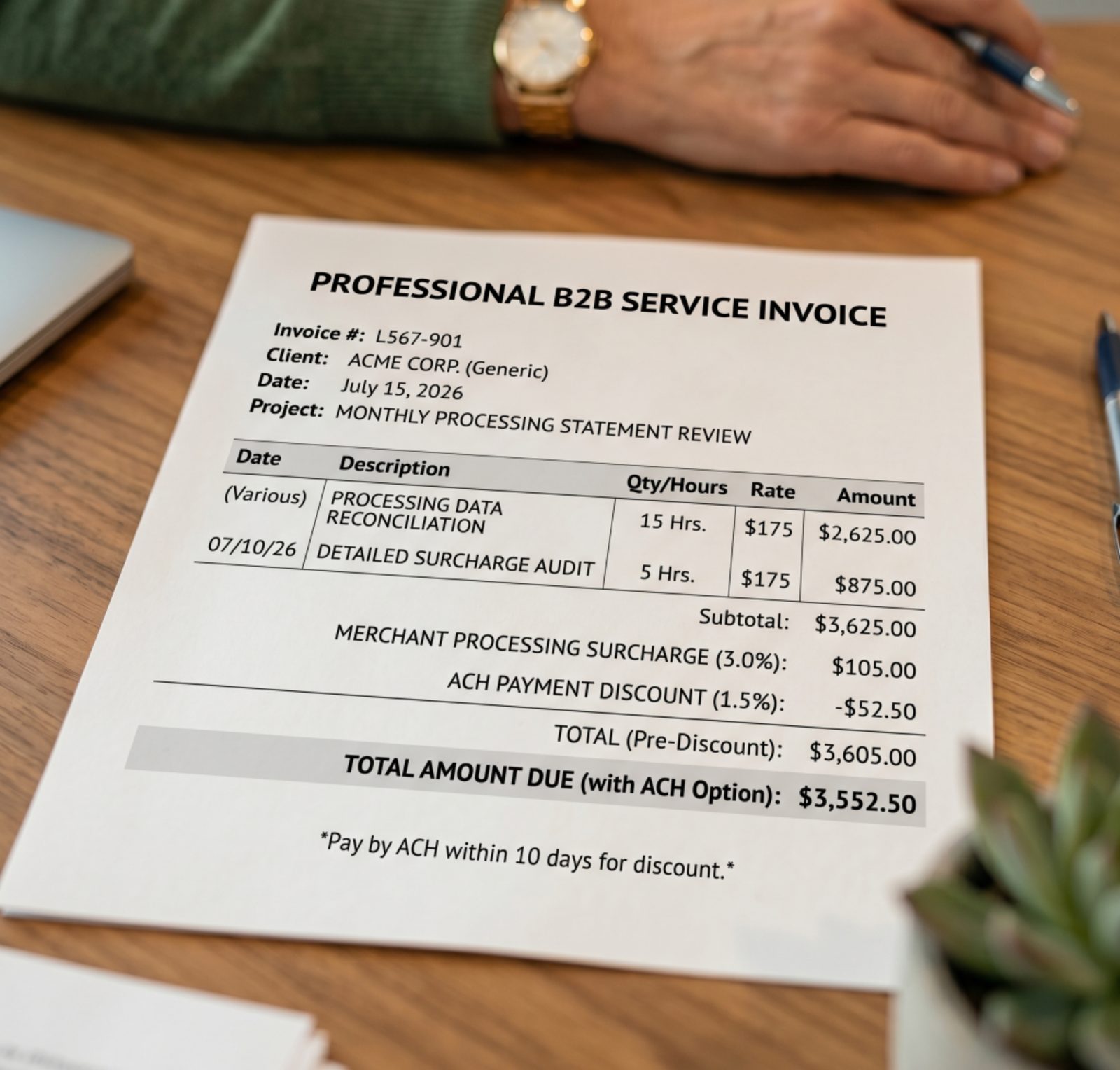

B2B businesses process large invoices by card every day. At 3%, the fees are significant. They don't have to be.

If your average transaction is $1,000, $5,000, or $20,000 — the math on processing fees is brutal. A single transaction can cost you $300 in fees. There's a legal, professional way to recover that cost.